Choosing the right insurance policy can be a daunting task. With so many types of insurance policies available in the market—each offering different coverage, benefits, and costs—it’s essential to understand what fits your unique needs, financial situation, and life goals. Whether it’s protecting your health, your loved ones, your property, or your income, the right insurance policy is a crucial pillar of financial security.

This article dives deep into various types of insurance policies, factors to consider when choosing one, and how to align insurance choices with your personal and financial goals. By the end, you’ll be equipped with enough knowledge to make informed decisions that provide peace of mind and financial protection.

Insurance is essentially a contract that transfers the risk of financial loss from an individual or business to an insurance company. The policyholder pays a premium, and in return, the insurer agrees to cover specific losses as outlined in the policy. The purpose of insurance is to provide peace of mind and financial security.

Introduction to Insurance

Insurance is essentially a contract that transfers the risk of financial loss from an individual or business to an insurance company. The policyholder pays a premium, and in return, the insurer agrees to cover specific losses as outlined in the policy. The purpose of insurance is to provide peace of mind and financial security.

There are many types of insurance policies, each designed to protect against different risks — from health emergencies to property damage to liability risks in business. Understanding what each policy covers and how it aligns with your personal or professional circumstances is crucial to making an informed decision.

Key Takeaways

- Insurance is a risk management tool tailored to different needs and circumstances.

- There are many types of insurance policies, each serving a specific purpose.

- Assess your risks, budget, and coverage needs before choosing a policy.

- Avoid common pitfalls by reading the fine print and reviewing policies regularly.

- Consult professionals if unsure, and always compare multiple offers.

- Which Insurance Policy Type Is Right for You?

Which Insurance Policy Type Is Right for You?

Expanded Introduction to Insurance

Insurance is often misunderstood as an unnecessary expense, but it’s a fundamental financial tool that protects you from potentially devastating financial losses. Whether it’s a sudden medical emergency, an accident, or the loss of a loved one, insurance acts as a safety net.

Consider this: According to the National Association of Insurance Commissioners (NAIC), the average American spends roughly 10% of their income on various types of insurance. This investment offers security that could save you from financial ruin during unforeseen events.

Understanding your insurance needs is the first step in protecting your financial future. This article will help you cut through the jargon and complexity.

Detailed Types of Insurance Policies

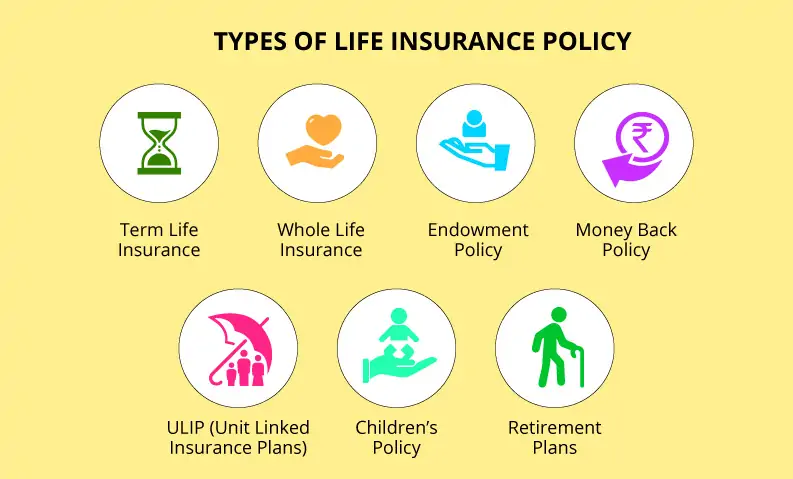

Life Insurance — More Than Just a Death Benefit

Life insurance is often viewed narrowly as a payout after death. But there’s more nuance to it:

- Term Life Insurance: Ideal for those seeking affordable coverage for a limited time, such as the duration of a mortgage or until children become financially independent. For example, a 30-year-old parent with young kids might opt for a 20-year term policy.

- Whole Life Insurance: Includes a cash value component that grows tax-deferred, offering a forced savings mechanism. For example, some policies allow policyholders to borrow against the cash value, which can be useful for emergencies or supplementing retirement income.

- Universal Life Insurance: Offers flexible premiums and death benefits, making it suitable for those with changing financial circumstances.

Example Scenario:

Jane, age 35, wants to ensure her children’s college expenses are covered if something happens to her. She chooses a 20-year term life insurance policy with a death benefit of $500,000. This provides affordable coverage for the critical years when her kids are young.

Health Insurance — Navigating Medical Costs

Medical expenses can quickly deplete savings without insurance. The average cost of a hospital stay in the U.S. exceeds $11,000, and chronic illnesses can rack up thousands annually in medications and treatments.

Key Health Insurance Terms:

- Premium: Your monthly payment.

- Deductible: Amount you pay out of pocket before insurance covers costs.

- Copay: Fixed amount you pay per visit or prescription.

- Out-of-Pocket Maximum: The most you pay in a year before insurance covers 100%.

Types of Health Plans:

- Health Maintenance Organization (HMO): Requires a primary care doctor and referrals. Lower cost but less flexibility.

- Preferred Provider Organization (PPO): More flexible with providers but higher premiums.

- High Deductible Health Plan (HDHP): Lower premiums, higher deductibles, often paired with Health Savings Accounts (HSAs).

Auto Insurance — Protection on the Road

Auto insurance is mandatory in most states but also provides critical financial protection:

- Liability: Covers injuries or property damage to others caused by you.

- Collision: Pays to repair your car after an accident.

- Comprehensive: Covers non-collision damage like theft or natural disasters.

- Uninsured/Underinsured Motorist: Protects you if the other driver lacks sufficient insurance.

Example:

John carries minimum liability insurance to meet state requirements, but he adds collision coverage to protect his newer car, understanding repair costs could be high.

Homeowners and Renters Insurance — Guarding Your Home and Belongings

Homeowners insurance covers structure damage and liability if someone is injured on your property. Renters insurance protects your belongings inside a rental and covers liability.

What’s Covered?

- Fire, wind, hail, theft, vandalism.

- Personal liability (legal costs if someone sues).

Not Covered:

Flood damage usually requires separate flood insurance.

Disability Insurance — Income Protection When You Can’t Work

Disability insurance replaces a portion of your income if illness or injury prevents you from working. According to the Social Security Administration, one in four 20-year-olds will experience a disability before retirement.

Short-Term Disability: Covers 3–6 months.

Long-Term Disability: Covers from 2 years to retirement age.

Long-Term Care Insurance — Planning for Aging

Long-term care insurance covers costs of nursing homes, assisted living, or in-home care. These costs can be astronomical; the median annual cost for a private nursing home room in the U.S. is over $100,000.

Travel Insurance — Peace of Mind When Abroad

Travel insurance covers trip cancellations, medical emergencies overseas, lost luggage, and travel delays. It’s especially useful for international or costly trips.

How to Determine Which Policy Is Right for You — Expanded Insights

- Evaluate Your Life Stage:

- Young singles may prioritize health and renters insurance.

- New parents might add life and disability insurance.

- Older adults should consider long-term care and review health coverage.

- Assess Your Financial Situation:

- Emergency fund size.

- Monthly income and expenses.

- Debt levels.

- List Your Assets and Liabilities:

- Mortgage, car loans, dependents’ needs.

- Consider Risks Specific to Your Location:

- Flood-prone areas need flood insurance.

- High traffic areas may require higher auto liability.

- Consult Professionals:

Financial advisors or insurance brokers can tailor recommendations.

Key Factors to Consider Before Buying Insurance — Deep Dive

- Premium Affordability: Never sacrifice critical coverage for cheap premiums.

- Coverage Gaps: Check for what’s excluded or limited.

- Claim Settlement Ratio: A higher ratio indicates insurer reliability.

- Policy Riders: Custom add-ons like critical illness or accidental death benefit.

- Renewability and Cancellation Terms: Will your policy renew automatically? Under what conditions can the insurer cancel?

Step-by-Step Guide to Choosing Your Insurance Policy — Detailed Walkthrough

- Identify your risks and coverage needs.

- Set a budget for premiums.

- Research insurance providers and policies.

- Request quotes and compare.

- Check financial ratings (A.M. Best, Moody’s).

- Review policy terms for limits and exclusions.

- Consult an insurance expert if needed.

- Make an informed purchase.

- Keep all policy documents safe.

- Review annually and after major life changes.

Key Types of Insurance Policies

Insurance policies come in many forms, each designed to protect you against specific risks. Understanding the key types of insurance policies allows you to identify which coverages you need to secure your financial future. Here’s a detailed look at the most common and important types of insurance:

Life Insurance

Purpose:

Life insurance provides a financial safety net to your beneficiaries (usually family members) after your death. It ensures they have financial support to cover living expenses, debts, education costs, and more.

Main Types:

- Term Life Insurance:

Provides coverage for a set number of years (e.g., 10, 20, or 30 years). It pays a death benefit only if you die during the term. This is usually the most affordable option. - Whole Life Insurance:

Offers lifetime coverage with a savings component known as cash value that grows over time. Premiums tend to be higher but remain fixed. - Universal Life Insurance:

Flexible policy with adjustable premiums and death benefits. It also includes a cash value component.

Who Needs It:

- People with dependents (children, spouse, aging parents).

- Those with significant debts or a mortgage.

- Individuals who want to leave an inheritance or cover estate taxes.

Health Insurance

Purpose:

Health insurance covers medical expenses including doctor visits, hospital stays, surgeries, prescription drugs, and sometimes dental and vision care.

Common Plans:

- Employer-Sponsored Plans: Provided through your job, often with some employer contributions.

- Individual/Family Plans: Bought independently if not covered by work.

- Government Programs: Medicare (for seniors), Medicaid (for low-income individuals).

Key Terms:

- Premium: Monthly cost.

- Deductible: Amount you pay before insurance kicks in.

- Copay/Coinsurance: Your share of medical costs.

Who Needs It:

- Everyone! Medical bills are a leading cause of bankruptcy without insurance.

Auto Insurance

Purpose:

Auto insurance protects you against financial loss in the event of a vehicle accident, theft, or damage.

Core Coverages:

- Liability Insurance: Covers injuries/damages to others you cause.

- Collision Insurance: Pays for damage to your vehicle from accidents.

- Comprehensive Insurance: Covers non-collision events (theft, fire, natural disasters).

- Uninsured/Underinsured Motorist: Protects you if the other driver lacks insurance.

Who Needs It:

- All vehicle owners/drivers; required by law in most places.

Homeowners Insurance

Purpose:

Homeowners insurance protects your home structure and personal belongings against risks like fire, theft, or natural disasters. It also provides liability coverage if someone is injured on your property.

Coverage Types:

- Dwelling Coverage: For physical damage to the house.

- Personal Property: Covers belongings inside the home.

- Liability: Covers injuries or damages to others on your property.

- Additional Living Expenses: Pays for temporary housing if your home is uninhabitable.

Who Needs It:

- Homeowners, especially those with mortgages requiring coverage.

Renters Insurance

Purpose:

Renters insurance protects the personal belongings of tenants and covers liability if someone is injured in the rented space.

What’s Covered:

- Personal property losses from fire, theft, or vandalism.

- Liability protection.

- Temporary living expenses if the rental becomes uninhabitable.

Who Needs It:

- Renters wanting to protect their possessions and liability.

Disability Insurance

Purpose:

Disability insurance replaces part of your income if you are unable to work due to injury or illness.

Types:

- Short-Term Disability: Covers a few months of income.

- Long-Term Disability: Covers longer periods, potentially until retirement.

Who Needs It:

- Anyone whose income depends on working, especially those without large savings.

Long-Term Care Insurance

Purpose:

Covers costs of extended care services, such as nursing homes, assisted living, or home care, which are not typically covered by regular health insurance or Medicare.

Who Needs It:

- Older adults or those planning ahead for aging care expenses.

Travel Insurance

Purpose:

Provides coverage for risks related to travel including trip cancellations, medical emergencies abroad, lost baggage, and travel delays.

Who Needs It:

- Frequent travelers, especially those taking expensive or international trips.

Liability Insurance (Personal and Umbrella)

Purpose:

Liability insurance protects you if you cause bodily injury or property damage to others.

Types:

- Personal Liability: Often part of homeowners or renters insurance.

- Umbrella Insurance: Provides extra liability coverage above the limits of your other policies.

Who Needs It:

- Anyone who wants additional protection against large liability claims or lawsuits.

Summary Table of Key Insurance Types

| Insurance Type | Purpose | Who Needs It | Common Features/Notes |

|---|---|---|---|

| Life Insurance | Financial protection for beneficiaries | People with dependents or debts | Term (temporary), Whole, Universal |

| Health Insurance | Medical cost coverage | Everyone | Premiums, deductibles, copays, networks |

| Auto Insurance | Vehicle damage/liability protection | Vehicle owners/drivers | Liability, collision, comprehensive |

| Homeowners Insurance | Protect home structure & belongings | Homeowners | Dwelling, personal property, liability |

| Renters Insurance | Protect personal belongings & liability | Renters | Personal property, liability, living expenses |

| Disability Insurance | Income replacement during disability | Working individuals | Short-term, long-term |

| Long-Term Care | Coverage for extended care services | Older adults/planners | Nursing homes, assisted living, home care |

| Travel Insurance | Coverage for travel-related risks | Travelers | Trip cancellation, emergency medical |

| Liability Insurance | Protection against liability claims | Anyone wanting extra liability protection | Umbrella policies extend liability limits |

Factors to Consider When Choosing an Insurance Policy

- Your financial situation — Can you afford the premiums?

- Risk factors — What risks do you face personally or professionally?

- Coverage needs — What do you need protection for?

- Policy limits and exclusions — How much will the insurer pay and what won’t they cover?

- Reputation of the insurer — Reliability, customer service, claim settlement record.

- Policy flexibility — Can you adjust coverage as your needs change?

How to Assess Your Insurance Needs

Start with a risk assessment: consider your assets, liabilities, dependents, health, and lifestyle. For example, a single young adult may prioritize health and auto insurance, whereas a parent might focus more on life and home insurance.

Common Mistakes to Avoid

- Underinsuring or overinsuring.

- Ignoring policy exclusions.

- Not reviewing your policy regularly.

- Choosing the cheapest option without considering coverage quality.

How to Compare Insurance Policies

- Check premiums, deductibles, and co-pays.

- Compare coverage limits.

- Read reviews and insurer ratings.

- Ask for quotes from multiple companies.

- Understand the claims process.

Step-by-Step Guide to Selecting Your Insurance Policy

- Identify what you need to insure.

- Determine your budget for premiums.

- Research insurance providers.

- Request quotes and compare policies.

- Read the fine print carefully.

- Consult a financial advisor if needed.

- Purchase the policy and keep your documents safe.

Also Read : Do You Really Need Home Insurance?

Conclusion

Choosing the right insurance policy is a vital step toward securing your financial future and protecting yourself and your loved ones from unexpected hardships. Insurance isn’t just about meeting legal requirements or ticking boxes—it’s about creating a personalized safety net tailored to your unique life situation, assets, and goals.

Whether it’s life insurance to support your family in your absence, health insurance to cover costly medical bills, auto insurance to protect your vehicle and comply with the law, or other types like disability, renters, or long-term care insurance, understanding what each policy offers is essential. No one policy fits everyone; your needs may change over time as your personal circumstances evolve.

Take the time to assess your risks, financial commitments, and priorities. Compare policies, read the fine print, and consider working with a trusted insurance advisor to find the best solutions. Remember, the right insurance policy not only provides peace of mind but also helps you avoid financial setbacks during life’s uncertainties.

Ultimately, informed decisions about insurance empower you to live confidently today while preparing wisely for tomorrow.

FAQs

Q1: Can I have multiple insurance policies for the same risk?

A: Yes, but coordination of benefits is important to avoid paying unnecessary premiums.

Q2: How often should I review my insurance policies?

A: At least once a year or after major life changes like marriage, buying a home, or starting a business.

Q3: What happens if I don’t have insurance?

A: You risk bearing the full cost of any loss or liability, which can be financially devastating.

Q4: Are insurance premiums tax-deductible?

A: It depends on the policy type and jurisdiction; for example, some business insurance premiums may be deductible.

Q5: How do deductibles work?

A: You pay out-of-pocket up to the deductible amount before insurance coverage kicks in.

Q6: What is the difference between term and whole life insurance?

A: Term provides coverage for a fixed period, while whole life covers you for your entire life and may build cash value.

Q7: Can I change my insurance policy after purchase?

A: Many policies allow adjustments or add-ons, but terms vary by insurer.